Insuring a custom bike can be confusing. What coverage do you need? Should you have an appraisal done? What’s Agreed Value? These are all questions that come up, and there’s very little information available on the web. What’s more, many agents have little experience selling policies for anything but modern, factory-spec bikes.

We’re going to try to keep your blood pressure down by covering as many aspects of the process as possible in one place, then provide you with a tool to find the best coverage for you.

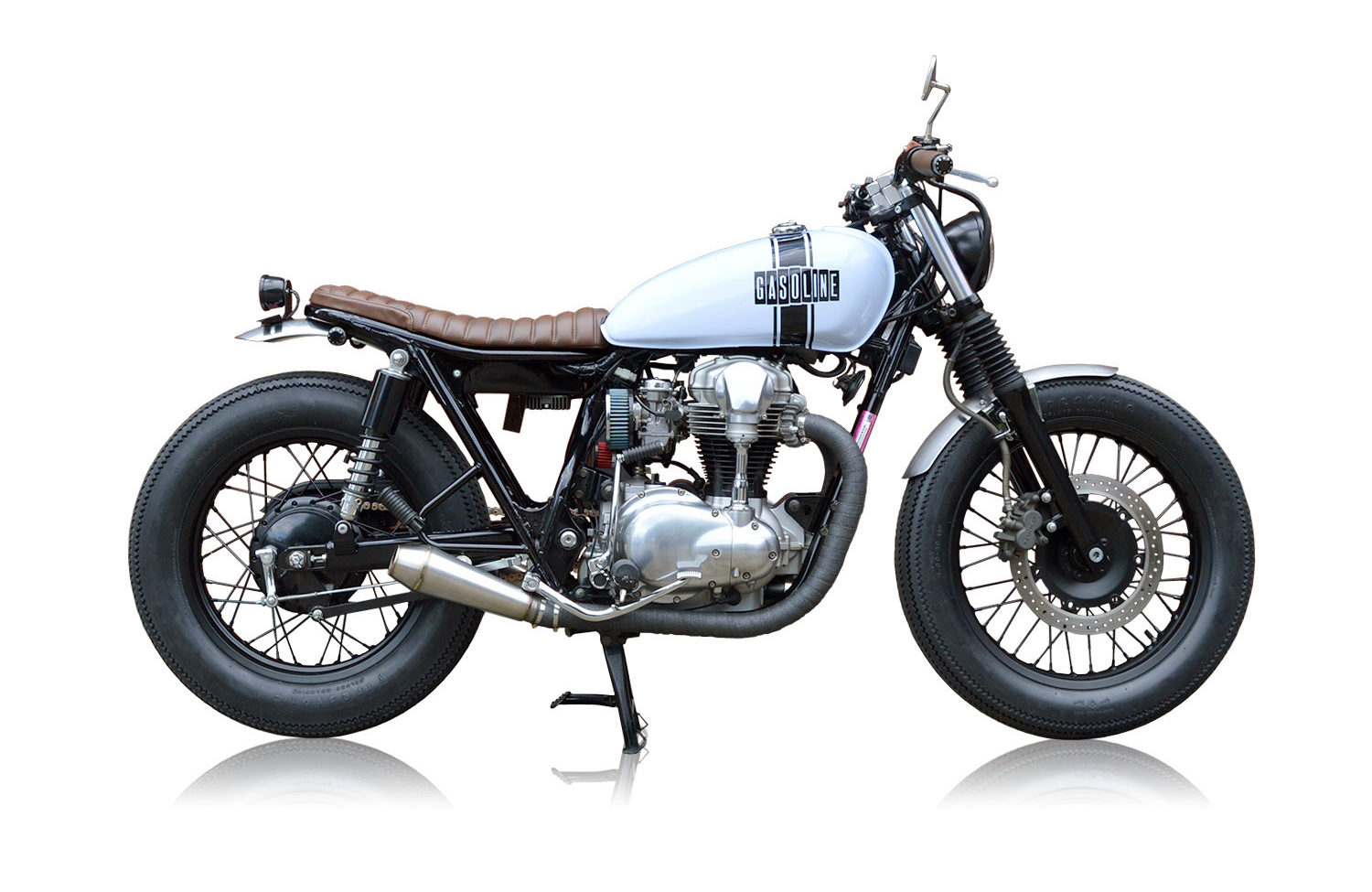

What Qualifies as Custom?

Sure, you have an image of a custom bike in mind. Your perspective may not be the same as someone else’s, so we compiled a list of bikes that may be categorized as custom.

- Bobbers

- Choppers

- Cafe Racers

- Scramblers

- Trackers

- Non-Factory Trikes

- Hybrids like the Triton, Tribsa, and Vincati

- Any custom-built or kit bike without a VIN number

The term ”custom motorcycle” covers nearly every bike that is not factory stock in significant ways. Whether you need specialized insurance for your bike comes down to its value if you need to replace it. That is where an appraisal and agreed value come into play.

Custom Motorcycle Coverage

Review Rates and Policies Online

Enter Zip Code

Agreed Value for Custom Motorcycles

If you own a custom motorcycle, you know that it’s worth far more than the sum of its parts. You also know how hard it was to come by some of those parts, especially the ones that will need to be handmade if they ever need to be replaced. In order to get full value after an accident or theft, you may want to get Agreed Value coverage. This is the amount that you and your insurance company agree it will cost to totally replace ride.

Typically, you indicate the value of your bike when submitting your application, and the insurer’s underwriters confirm this amount, making sure you’re not over- or under-insured. They may request receipts for parts and labor, or photos of the bike. You agree to maintain coverage of that amount, while the insurance company agrees to pay out the Agreed Value in the event of a total loss–minus your deductible or salvage value if you keep the bike. The Agreed Value can be increased as you upgrade and modify your bike.

Appraisals for Custom Motorcycles

In some cases, you may have to have your bike appraised. An appraisal will reflect both the cursory cost to modify your bike and its fair market value. An appraisal is important not only for insurance purposes, but equity evidence and estate settlement as well. Bottom line: the appraised value is current fair market value, or ”actual cash value” (A.C.V.) in insurance company lingo.

When appraising a custom motorcycle, a number of factors are taken into consideration. Primarily, the appraisal is used to reconcile the modifications and aftermarket parts, justifying the invested amount of the bike. After that, the appraiser will compare your build to other bikes based on year, make, model, and caliber. These are called comparative offerings.

Typically, an appraisal is not necessary unless it’s a kit or ground-up, custom-built bike.

Custom Parts and Equipment Coverage (CPE)

Agreed value policies are typically for bikes at least 25 years old. For newer bikes, a company may use an array of coverage types to insure your aftermarket parts and modifications. Beyond the standard comprehensive, collision, and various medical payment insurance policies, you may need to carry Custom Parts and Equipment Coverage (CPE) and/or Additional Parts and Equipment Coverage (ACPE).

According to Allstate, custom parts and equipment coverage (CPE) is an addition to your policy that covers…

“Custom parts or equipment; devices; accessories; and any enhancements and changes other than those installed by the original manufacturer that alter the performance or appearance of your vehicle and are permanent in nature.”

The coverage is separate from your collision and comprehensive coverage, but it may have the same deductible.

Additional parts and equipment coverage (ACPE) is another addition to your policy that only kicks in if you have a pre-determined value invested in custom parts. The usual starting amount is $1,000, but can vary by insurer. This coverage may be a subset within CPE with some companies. In essence, it opens an avenue for the insurer to pay for your expensive specialty parts.

Who Insures Custom Motorcycles?

Many of the top insurance companies in the United States offer custom motorcycle insurance, and there several small specialty insurers that insure custom and vintage bikes as well. Here is a short list of companies that offer this type of coverage:

- Allstate

- Nationwide

- Progressive

- Fischer Specialty

- Hagerty

- State Farm

- Geico

- Dairyland

- Rider

If your frame has an MSO (Manufacturer Statement of Origin) instead of a VIN, some of the larger insurers like Allstate can look these up in their systems. Keep in mind that this is a short list of the companies that offer custom motorcycle insurance. Can you imagine how much time you would have invested in shopping around for the best coverage? That’s why we offer a convenient tool where you can request and compare quotes from insurers in your area…online!

Get Coverage Online

Review Rates and Policies Online

Enter Zip Code

More Information

If you want some inspiration for your custom build, we encourage you to peruse the array of custom motorcycles we’ve featured on the blog. If you have a kit build or frame with an MSO, this thread on the S&S Cycle forum might be helpful.